March 2026 has delivered more change for Australian property investors than most months in recent memory. The RBA lifted the cash rate to 4.1% on 17 March, the second consecutive hike decided by a narrow 5-4 board vote. A Senate committee delivered its final report formally recommending changes to the CGT discount. The Treasurer publicly pledged an ambitious May budget. And this morning, the ABS released the February CPI data. We have gone through all of it and here is what it means for investors.

Key highlights

- RBA cash rate lifted to 4.1% on 17 March, second consecutive 25bp hike, decided 5-4

- February CPI: headline 3.7% (down from 3.8%), trimmed mean steady at 3.3%

- Housing group: +7.2% annually, the dominant inflation driver since July 2025

- Electricity: +37.0% annually, up from 32.2% in January

- Rents: +3.8% annually, re-accelerating after bottoming at 0.4% in June 2025

- Perth housing CPI: +14.8% annually, more than double the national average

- Consumer inflation expectations: 5.2% in March, highest since July 2023

- Senate committee final report formally recommends reducing the 50% CGT discount

- Treasurer Chalmers confirms Treasury is drafting CGT, negative gearing and trust changes for May budget

- Auction clearance rates fell to lowest point of 2026 (57.9% revised final for one week)

The rate picture: two hikes down, more likely ahead

The RBA's decision on 17 March was widely expected but no less significant for that. The board voted 5-4 to lift the official cash rate to 4.1%, the second consecutive 25 basis point increase following February's hike. Variable rates for many investment mortgage holders are now pushing above 6%. The two hikes combined add roughly $225 per month to repayments on a $700,000 loan, or about $2,500 per year on a $500,000 investment mortgage before the tax deduction.

In its statement, the board cited persistent capacity pressures in the domestic economy and the inflationary impact of rising fuel prices from the Middle East conflict. Governor Michele Bullock was direct in her post-meeting press conference: demand is outstripping supply, and inflation is too high. The board flagged it will remain data-dependent but left no doubt that further tightening remains on the table.

Most major bank economists now have a third hike at the May meeting as their base case. Consumer inflation expectations rose to 5.2% in March, the highest reading since July 2023, which the RBA monitors closely as a leading indicator of wage and price-setting behaviour. If expectations become entrenched, the board's hand is further forced.

"The economy grew faster than its potential growth rate over the second half of last year, the labour market has tightened a little recently, and underlying inflation remains high." - RBA Governor Michele Bullock, March 2026

The February CPI: what the data actually shows

The February CPI data released this morning shows headline inflation at 3.7%, a marginal easing from 3.8% in January. At first glance that looks like progress. It is not quite what it seems.

The RBA's preferred underlying measure, the trimmed mean, held steady at 3.3%, unchanged from January. The headline easing is largely explained by a single factor: automotive fuel fell 7.2% in the 12 months to February, data collected before the Middle East conflict pushed oil prices sharply higher. That effect will reverse in the March CPI print, due 29 April, and most economists expect the March read to come in noticeably higher.

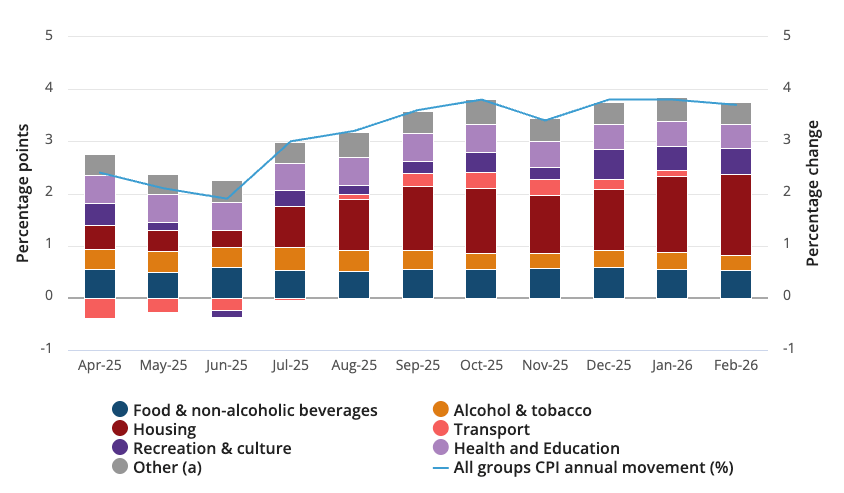

Housing is driving inflation

CPI Groups, contribution to annual CPI movement (percentage points)

Source: ABS Consumer Price Index, Australia, February 2026

Strip out the fuel effect and the picture is one of persistent, domestically-driven inflation. Housing is the dominant contributor, rising 7.2% annually in February, up from 6.8% in January and from a contribution of just 0.80 percentage points in July 2025 to 1.55 percentage points by February 2026. No other CPI group comes close.

Within the housing group, three components are doing the work:

- Electricity: +37.0% annually. The jump from 32.2% in January reflects the cessation of Commonwealth and state government energy rebates. Excluding the rebate effect, underlying electricity prices rose 4.9% annually. The important point for investors: this is the single largest cost pressure tenants are absorbing right now.

- New dwellings: +3.7% annually. Project home builders are passing through higher labour and materials costs. This matters for the supply story: rising construction costs reduce developer feasibility and constrain the housing pipeline, which means the existing undersupply is not being resolved.

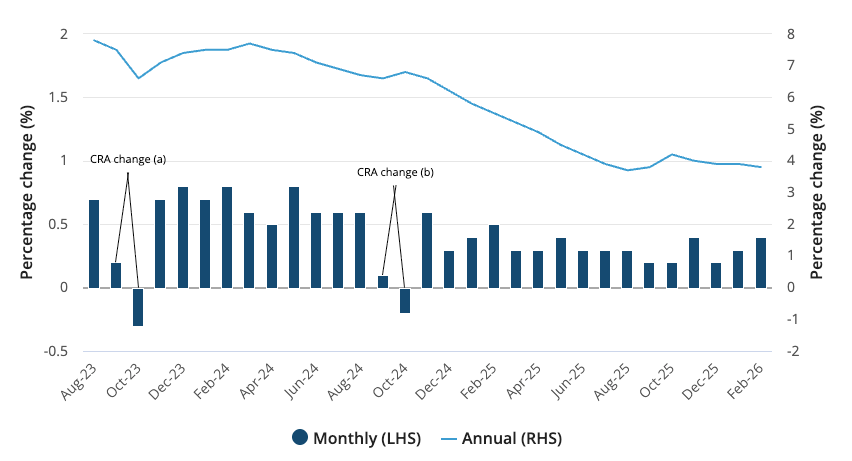

- Rents: +3.8% annually. After bottoming at just 0.4% annual growth in June 2025, rental inflation has re-accelerated consistently for eight months. The ABS notes this reflects sustained low vacancy rates in most capital cities.

Rents, Australia, monthly and annual movement (%)

Source: ABS Consumer Price Index, Australia, February 2026

The rent re-acceleration is the most important signal for landlords in this report. It means the period of soft rental growth is over. Tight vacancy, strong population growth, and a construction pipeline that cannot keep pace with demand are combining to push rents higher. For investors holding residential property, that is a genuine cashflow tailwind.

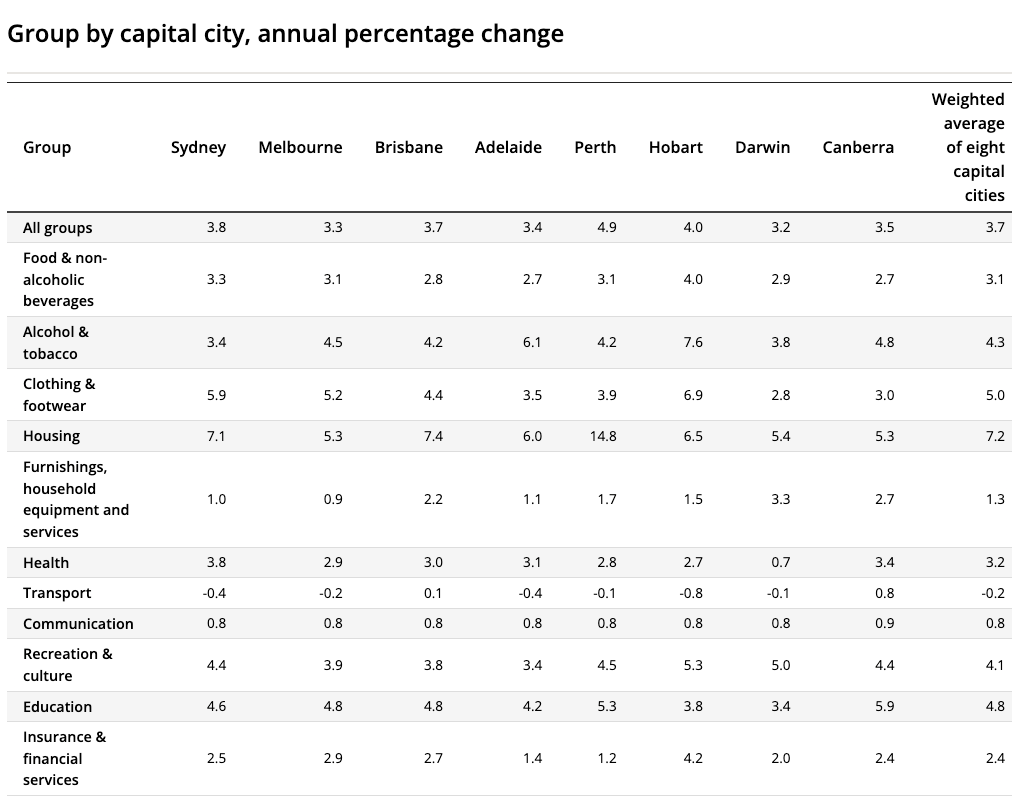

Perth stands out

The city-by-city breakdown reveals significant variation across markets. Perth's housing CPI rose 14.8% annually, more than double the national average of 7.2%. Brisbane recorded 7.4%, Adelaide 6.0%, and Sydney 7.1%. Melbourne and Darwin came in lower at 5.3% and 5.4% respectively.

Perth's figure reflects an exceptionally tight rental market, strong interstate and international migration, and a mining-led economy that continues to generate demand. For investors in Perth or considering the market, it is a strong structural signal.

14.8% Housing CPI annual growth in Perth (Feb 2026). National average: 7.2%.

Source: ABS Consumer Price Index, Australia, February 2026

The structural tension the RBA cannot fix

There is a problem at the heart of the current policy approach that is worth understanding clearly. Housing is the dominant driver of inflation. Yet rate hikes increase borrowing costs for developers, reduce construction feasibility, and slow the pipeline of new supply. Raising interest rates to reduce housing inflation makes new housing more expensive to build. You cannot fix a supply-side problem with a demand-side tool.

The RBA knows this. Governor Bullock told parliament earlier this year she is not confident housing supply will improve for at least two years. The policy tool in use is the only one the RBA has available, but its effectiveness in addressing the specific drivers of current inflation is limited. For existing landlords, that supply constraint is a structural tailwind for both property values and rental income.

"Australia's rental market is reaching the point where renters simply can't afford to pay much more, even though competition remains strong. Rents are still at record highs, but household budgets are under pressure." - Dr Nicola Powell, Domain chief of research and economics

The CGT and negative gearing picture has crystallised

When we covered the proposed CGT and negative gearing changes in earlier market updates, these were proposals being modelled. In the last week, the picture has shifted considerably toward certainty.

The Senate committee inquiry into the CGT discount delivered its final report last week. The majority finding was explicit: the current concessions, combined with negative gearing, have the potential to distort investment allocation and have skewed housing ownership away from owner-occupiers toward investors. That is a formal Senate recommendation, not a think-tank submission.

Within days, Treasurer Jim Chalmers gave a public speech pledging an ambitious May budget, with confirmed reports that Treasury is actively drafting changes to the CGT discount, negative gearing, and trust structures. The Treasurer framed the reforms as helping younger generations and driving stronger investment, and warned of hard decisions ahead given the Middle East-driven economic uncertainty.

What the most credible scenario looks like

The scenario with the strongest cross-party support is a reduction of the CGT discount from the current 50% to somewhere between 25% and 33% for assets held longer than 12 months. The Greens and independent senators David Pocock and Allegra Spender have all publicly backed versions of this change. The Senate arithmetic gives the government a viable path to legislating it.

Grandfathering provisions are widely expected. Under the likely design, the relevant date would be the contract date on a new property purchase, not settlement. Properties purchased before the legislation commences would be expected to retain the current 50% discount for their lifetime. Properties purchased after would be subject to the new, lower discount.

The dollar difference is meaningful. On a $400,000 capital gain at the top marginal rate of 47%, the difference between a 50% and a 25% discount is approximately $47,000 in additional tax at the point of sale. That is a real number that changes investment planning.

$47,000 Additional tax at sale on a $400K capital gain if CGT discount reduces from 50% to 25% at the top marginal rate.

Illustrative calculation only. Investors should seek independent tax advice for their specific circumstances.

What it means for the investment calculus

A reduced CGT discount does not make property investment unworkable. But it does change which strategies outperform. The current settings allow investors to run a negatively geared property, deducting annual losses at their full marginal rate, then pay tax on only half the gain when they sell. That arbitrage becomes less attractive when the discounted gain is taxed at a higher effective rate.

The strategic implication is a shift toward income over gain. Properties with strong rental yield, quality tenants, and low vacancy become more valuable relative to low-yield, high-growth plays. Investors who build genuine rental income rather than relying primarily on a discounted capital gain at exit are better positioned under either tax scenario.

What investors are moving on right now

Across the conversations we are having with investors and brokers, a few themes are coming through consistently.

Acting before the budget cut-off

The pre-budget window is explicitly time-sensitive in a way it has not been before. If grandfathering provisions apply from the contract date, a property purchased before the legislation takes effect keeps the current 50% discount for its lifetime. The May budget date is the practical deadline. For investors who have been considering a further purchase, the tax argument for acting before May is now concrete rather than theoretical.

The constraint is usually having the deposit available quickly. A bank approval takes 4 to 8 weeks. Futurerent can advance up to $100,000 per investment property in 2 business days, without touching the existing mortgage, without income verification, and without a credit impact.

Moving in a softer market

Auction clearance rates across the combined capitals fell to their lowest point of 2026 last week, with one week's result revised down to 57.9% after re-weighting. Sydney and Melbourne are showing the clearest impact from the two rate hikes. This is not a bear market. But it is a less competitive one. Buyers with capital ready are finding they can get better quality properties for less and this is the key factor that often gets buried in the data until it looks like an obvious bargain in hindsight.

Accessing equity without going back to the bank

The cost of a cash-out refinance has increased significantly with each rate hike. Variable rates above 6% mean that restructuring a mortgage to access equity is the most expensive it has been since late 2023, and potentially heading higher. For investors who want access to capital without altering their existing loan structure, rate, or lender relationship, Futurerent provides a direct alternative that the current rate environment makes increasingly competitive.

Upgrading for yield

Today's inflation data is showing rents and construction costs increasing significantly and this trend is likely to continue. Rents re-accelerated to 3.8% annually after bottoming at just 0.4% in mid-2025. That re-acceleration is a direct positive cashflow signal for landlords — not a temporary blip but a sustained eight-month trend driven by vacancy rates that remain structurally low.

Rising construction costs are likely to make it even more difficult to bring more supply to market, placing more pressure on prices. This matters because it reframes what is happening with inflation. Housing is driving inflation. Rate hikes increase construction finance costs and reduce developer feasibility. The tool being used to fight the inflation is the same tool making the supply problem worse. For investors already holding property, both the rent trend and the supply constraint are working in their favour.

"Property investors know that prices grow faster than you can save. And even with a foot on the property ladder, taking the next step shouldn't mean asking the bank's permission, changing your entire mortgage and signing up to another lifetime of interest when all you need is to unlock what's already yours."

How Futurerent can help

The current environment rewards investors who can move quickly and stay flexible. Two rate hikes in two months, a tax change heading toward May, and a softer-but-not-broken auction market all create moments where the difference between acting and waiting is access to capital.

Futurerent helps property investors cash out up to $100,000 per investment property in 2 business days, without refinancing, without paperwork, and without affecting their credit score or existing mortgage. The advance is repaid from a fixed portion of rental income over three years. The property returns the cash out, not your wallet.

If you want to know what you can access on your investment property, use the calculator below or reply with the property address, weekly rent, and rough mortgage balance. We will come back with indicative numbers on what is available, the total fixed cost, and the cashflow impact. No commitment required.

Source: ABS Consumer Price Index, Australia, February 2026 (released 25 March 2026); RBA Statement on Monetary Policy March 2026; Senate committee inquiry into CGT discount, final report March 2026.