National property values jumped 0.7% in August, marking the strongest monthly gain since May 2024 and the seventh consecutive month of growth. With auction clearance rates hitting 76.3% across more than 2,200 scheduled properties and listings tracking 20% below historical averages, spring conditions are shaping up to deliver significant opportunities for investors.

Spring Season Arrives

Australia's property market has entered Spring with strong momentum, delivering its strongest monthly performance in over a year as buyers position themselves ahead of what promises to be an exceptionally active spring selling season.

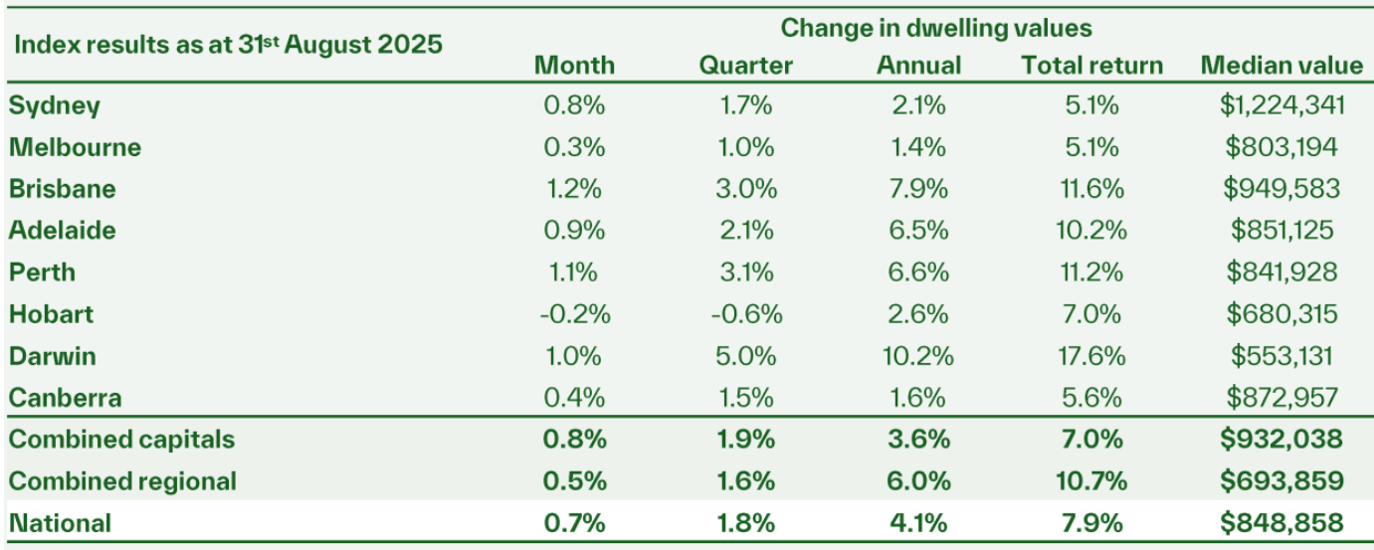

The 0.7% national dwelling value increase through August represents a clear acceleration from previous months, pushing the national median to $848,858 and annual growth to 4.1%. This marks the seventh consecutive month of gains since the rate cutting cycle began in February, creating the sustained upward trajectory that many analysts predicted would emerge.

What makes August particularly significant is the confluence of factors supporting continued growth. The Reserve Bank's third rate cut to 3.60% is flowing through to improved borrowing capacity, while auction markets are demonstrating the kind of competitive tension that typically characterises strong property cycles.

Consumer sentiment has reached a 3½ year high in August, providing the psychological foundation for sustained buyer activity. The Westpac-Melbourne Institute survey's "time to buy a dwelling" index has climbed to levels not seen since 2021, while three-quarters of consumers now expect home prices to rise over the next 12 months.

With the federal government's expanded First Homebuyer Guarantee scheme launching October 1st, bringing unlimited eligible buyers into the market, August's momentum suggests we're witnessing the early stages of renewed market activity rather than a temporary uptick.

Cotality's research director Tim Lawless notes the supply-demand imbalance: "Once again we are seeing a clear mismatch between available supply and demonstrated demand placing upwards pressure on housing values."

Key Highlights

- National dwelling values rose 0.7% in August – strongest monthly gain since May 2024 and seventh straight month of growth

- Auction clearance rates hit 76.3% across 2,251 scheduled properties – highest volume since early June

- Sydney clearance rates broke 80% for first time since April 2024, reaching 80.3% with 825 auctions

- Melbourne recorded 74.9% clearance rate with 1,124 scheduled auctions, up 14.1% week-on-week

- National median dwelling value reaches $848,858 with annual growth accelerating to 4.1%

- Advertised listings remain 20% below seasonal averages at 120,000 vs typical 150,000 properties

- Brisbane median approaches major milestone at $949,000, closing in on $1 million mark

- Rental vacancy rates hold at 1.5% – near record lows compared to 3.3% pre-2020 average

Seventh Month Growth

Australia's property recovery has maintained steady momentum, with August's 0.7% gain representing the strongest monthly result in over a year and the seventh consecutive month of positive growth since February's initial rate cut.

This sustained momentum distinguishes the current cycle from the volatility that characterised previous periods. Rather than the sharp peaks and troughs seen during pandemic-era market movements, we're witnessing what appears to be a more measured and sustainable growth trajectory.

The 4.1% annual growth rate has now accelerated for two consecutive months, suggesting the positive trend is gaining strength rather than plateauing. At $848,858, the national median dwelling value reflects steady appreciation driven by fundamental supply-demand dynamics rather than speculative excess.

Sales activity demonstrates the strength of underlying demand, with the annual trend in estimated home sales up 2% on last year and tracking almost 4% above the previous five-year average. This performance occurs despite affordability constraints, indicating genuine buyer commitment in the current environment.

Monthly Change in dwelling values as at 31 August 2025

Eliza Owen, head of research at Cotality, explains the drivers behind this sustained growth: "You've got more demand in the housing market, with real wages growth up to its highest level in five years, lower interest rates and more consumer confidence aiding housing purchases. But on the supply side, more hesitancy from sellers through the start of the year means that listing volumes are pretty low."

The broad-based nature of this recovery, with growth evident across multiple capital cities and market segments, indicates the current cycle has strong foundational support that extends well beyond short-term sentiment shifts.

Change in dwelling values as at 31 August 2025

Auction Momentum

Spring selling season has arrived with authority, as auction markets delivered their strongest performance in months with preliminary clearance rates reaching 76.3% across 2,251 scheduled properties – the largest auction volume since early June.

This represents a full percentage point improvement from the previous week and signals growing vendor confidence as spring traditionally brings increased market activity. The 2,200+ scheduled auctions mark a significant increase in vendor willingness to test market conditions ahead of the traditionally busy spring period.

Sydney led the charge with preliminary clearance rates breaking the 80% threshold for the first time since April 2024, reaching 80.3% across 825 scheduled auctions. This 13.2% increase in auction volume week-on-week demonstrates renewed seller confidence in the harbour city's market conditions.

Melbourne maintained strong momentum with 74.9% clearance rates across 1,124 scheduled auctions, representing a substantial 14.1% increase in auction volume. While the clearance rate slipped slightly from previous weeks' 75%+ results, the significant increase in properties going to auction suggests vendors are confident about achieving strong results.

The smaller capitals showed mixed but generally positive results. Brisbane recorded a 64.5% clearance rate across 124 auctions, Adelaide achieved 75% across 106 properties, and the ACT delivered 76.7% across 63 scheduled auctions.

Tim Lawless notes the forward momentum building in auction markets: "Auction activity is set to reduce a little next week, with around 2,150 events scheduled, rising to about 2,400 the week after."

Dan White, managing director at Ray White Group, observes strong forward bookings: "There are some incentives coming in, which should underwrite the market to a certain degree. Conditions should be pretty steady into Christmas."

City Performance Analysis

The August results revealed interesting variations across capital cities, with some markets accelerating while others showed signs of moderation after strong previous performance.

Melbourne is demonstrating clear signs of recovery momentum, with dwelling values climbing steadily as the Victorian capital benefits from improved relative affordability. Houses in Melbourne are around the cheapest they have been relative to Sydney in two decades. The city's performance marks a significant turnaround from the slower conditions observed through late 2024, with strong population growth and competitive pricing attracting buyers back to the market.

Sydney's results reflect a mature market finding its rhythm, with the 0.8% monthly gain and 2.1% annual growth indicating steady appreciation rather than dramatic swings. The harbour city's performance suggests stability has returned after earlier volatility.

Brisbane continues its impressive trajectory, with the median dwelling value now sitting at $949,000. The Queensland capital's steady progress reflects ongoing interstate migration and relative affordability compared to Sydney and Melbourne.

Darwin and Perth continue to show leadership in growth terms, though the pace has moderated from earlier peaks as these markets transition to more sustainable trajectories. Darwin's performance remains particularly noteworthy given its relatively small market size and the outsized impact that demand shifts can have.

Adelaide recorded solid results with its 0.9% monthly gain, while the ACT and Hobart posted more modest but still positive growth, demonstrating the broad-based nature of the current recovery across Australian property markets.

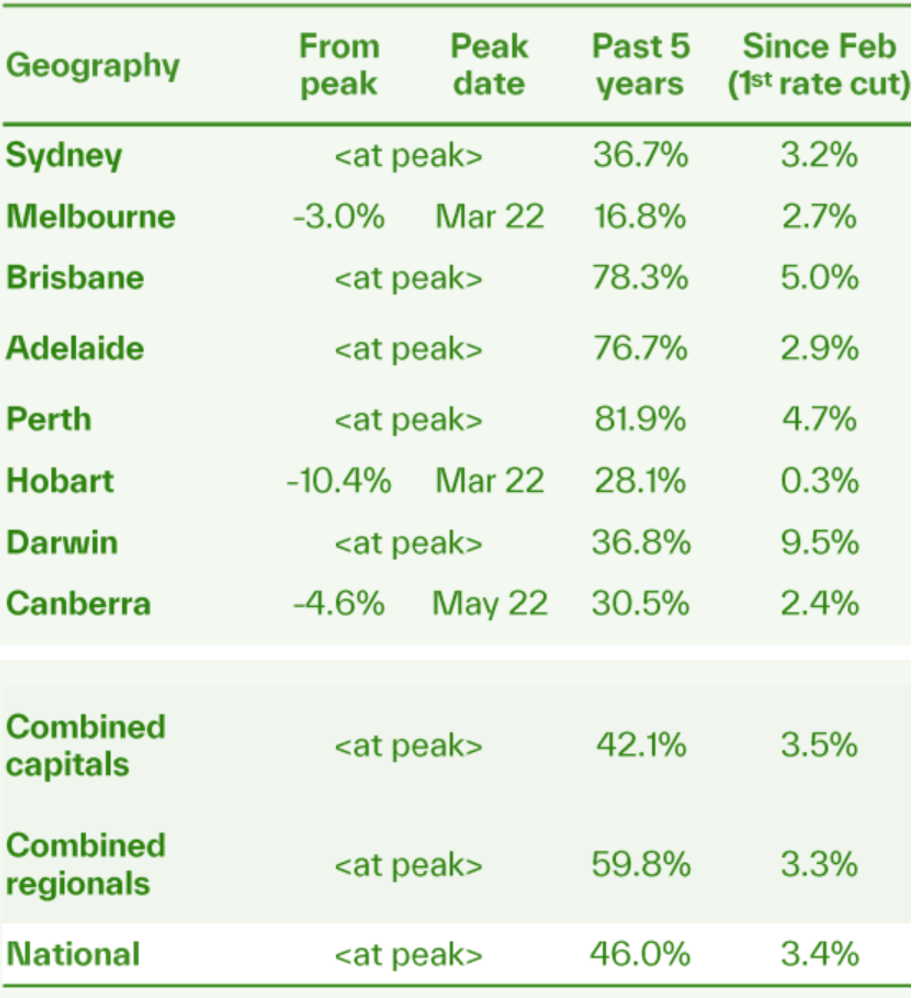

Change in Dwelling Values Over Key Time Periods

Rental Market Dynamics

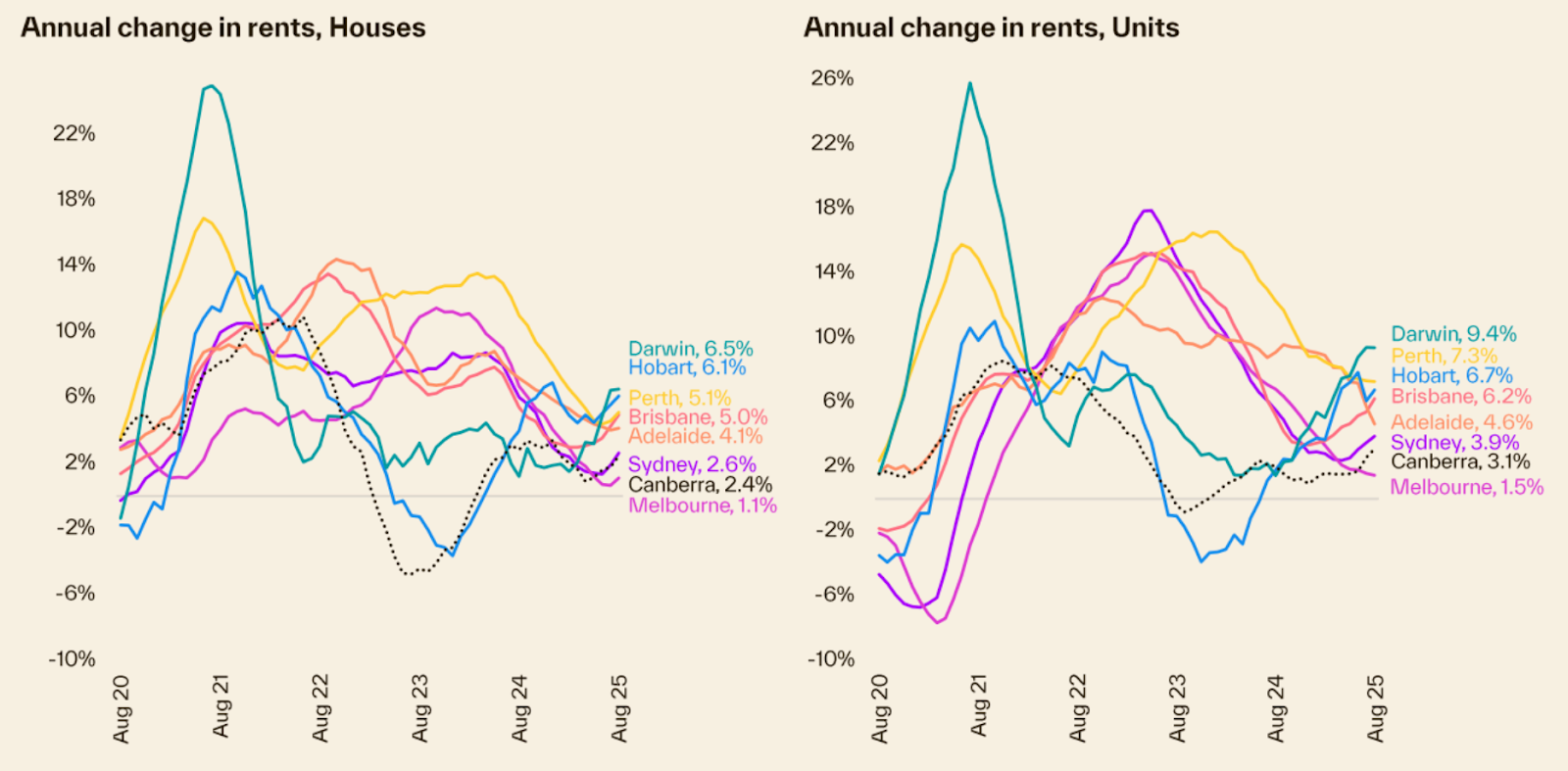

Australia's rental market continues to tighten, with national vacancy rates holding at 1.5% in August compared to the 3.3% average recorded in the five years prior to 2020. This near-record low vacancy environment is driving rental growth acceleration, with national rents recording 0.5% monthly growth through August – the fastest pace since May last year.

Annual rental growth has now reached 4.1%, with the trend strengthening across most capital cities. Darwin leads rental growth among capitals, with house rents up 6.5% over the past year and unit rents climbing 9.24% annually. This strong rental performance supports Darwin's impressive 6.5% gross rental yield across all dwellings.

The rental market variations across capitals reflect different supply-demand dynamics. Sydney remains home to the highest rental rates nationally, with median house rents at $833 per week and units at $749 per week. In contrast, Hobart offers the most affordable capital city rents, with typical houses renting for $603 per week and units for $506 per week.

Melbourne, the ACT and Sydney are recording softer rental growth conditions, with annual rent increases running below other capitals over the past 12 months. However, the underlying trend appears to be strengthening in these cities as well.

Tim Lawless warns of broader economic implications: "The reacceleration in market rents is one to watch considering the large weight allocated to rental prices in the CPI. There is more than a year of lag between rental value estimates and CPI rents paid, but if this uptick in rental growth continues it could gradually place some upwards pressure on inflation."

Annual change in rents (houses and units)

Demand Acceleration

Consumer sentiment has reached a 3½ year high in August, providing the psychological foundation for sustained buyer activity. The Westpac-Melbourne Institute survey's "time to buy a dwelling" index has climbed to levels not seen since 2021, while three-quarters of consumers now expect home prices to rise over the next 12 months.

Buyer activity is strengthening across key markets, with enquiry data showing robust demand momentum as we enter the spring selling season.

Darwin stands out with buyer enquiries per listing surging almost 50% compared with the same period last year, the highest increase of any capital city. In a relatively small market like Darwin, such demand shifts typically translate quickly into price appreciation and competitive auction conditions.

Key enquiries per listing by capital city (houses)

Melbourne has experienced a remarkable turnaround, with demand strengthening across more than 90% of its suburbs and enquiries up an average of 23% year-on-year. This represents a significant reversal from the softer conditions that characterised much of 2024, highlighting how lower interest rates and improved relative affordability are reigniting buyer interest.

Hobart has also recorded meaningful improvement, with enquiries rising nearly 30% year-on-year. This marks a significant shift after the Tasmanian capital experienced softer market conditions in recent years, demonstrating how the combination of lower interest rates and constrained supply is creating renewed competition.

Real wages growth at 1.3% annually represents the highest level since June 2020 and is about 2½ times the pre-COVID decade average of just 0.5%. This wage growth improvement, combined with the unemployment rate holding around 4% since late 2021, creates favourable conditions for loan serviceability and buyer confidence.

After drawing down on savings accumulated through the pandemic, households are once again managing to accrue savings, with the household saving ratio trending towards pre-pandemic averages. While higher savings also imply less consumption, a return to savings accumulation helps prospective buyers access the credit necessary for home purchases.

The annual trend in estimated home sales is up 2% on last year and tracking almost 4% above the previous five-year average, demonstrating that buyer activity is exceeding historical norms even in a supply-constrained environment.

Policy Catalyst

The federal government's announcement of the expanded First Homebuyer Guarantee scheme represents a significant demand-side stimulus that will reshape spring market dynamics from October 1st. The policy has been brought forward by three months from its original January 2026 implementation date, positioning it to launch just as spring selling season gains momentum.

The scheme's expansion removes previous income restrictions and increases eligible buyers from 35,000 to unlimited places, subject to property price caps. This enables buyers to purchase homes with just a 5% deposit without paying lenders' mortgage insurance, delivering savings of $5,000 to $30,000 per transaction depending on deposit size and property value.

The timing creates both opportunity and urgency. Independent analysis suggests this shift could bring forward purchasing decisions for between 20,600 and 39,100 buyers in the first year, adding substantial demand to an already supply-constrained market just as seasonal activity traditionally peaks.

Tim Lawless explains the deposit barrier this addresses: "Saving for a deposit is one of the biggest hurdles for accessing home ownership. Saving a 5% rather than a 20% deposit could shave around 10 years off the time it takes to accrue a deposit in an expensive market like Sydney."

"If I was to put myself in the shoes of a prospective first home buyer, I'd be trying to get into the market now before the expanded deposit guarantee went live, just to try to benefit from what's likely to be a wave of capital gain that flows through", he said.

Economist Nicholas Gruen warns of the immediate market impact: "If you stand in the marketplace and say, 'if you were saving up for a 20 per cent deposit, you don't need to any more, just sign here', then you will pull forward a lot of demand. That's the effect that produces the house price response in the short term."

The policy change comes at a time when borrowing capacity is already improving due to rate cuts, creating a compounding effect on buyer demand. NAB executive Matt Dawson observes: "The reality is many people assume they can't buy a home because they don't have a 20 per cent deposit. The scheme shows that homeownership can happen much sooner than expected."

Listing Volume Shortage

The fundamental listing supply shortage that has characterised Australia's property market continues to intensify, with listing volumes remaining substantially below historical norms even as spring selling season traditionally brings increased stock to market.

Current advertised listings sit at approximately 120,000 properties nationally, representing a 20% deficit compared to the typical 150,000 properties expected for this time of year. This persistent shortage occurs despite the seasonal uptick that normally accompanies spring market activity. So rising demand against tight supply is continuing to see a rise in home values.

Godfrey Dinh, CEO of Futurerent, observes: "We've got 120,000 properties listed when we'd normally see 150,000, while sales track nearly 4% above historical averages. The expanded guarantee will add significant buyer numbers to an already constrained market.

Tim Lawless acknowledges the seasonal expectations: "We are starting to see the usual start of spring upswing in new listings coming to market, but from a low base. A pick up in the flow of stock coming to market through spring will be good news for buyers who generally have limited choice at the moment."

However, the combination of low starting inventory levels and increasing buyer competition suggests that even normal seasonal increases in listings may not be sufficient to restore market balance. This dynamic creates ongoing support for price appreciation as buyers compete for limited available properties.

The rental market reflects similar supply constraints, with national vacancy rates holding at 1.5% compared to the 3.3% average recorded in the five years prior to 2020. This tight rental market provides additional pressure on potential buyers to transition from renting to ownership where possible.

Strategic Implications

The convergence of multiple positive factors creates compelling conditions for property investors who can move decisively ahead of increased spring competition.

Current market dynamics favor investors with flexible funding arrangements and the ability to act quickly. With auction clearance rates at their highest levels since early 2024 and listings remaining 20% below average, properties that meet investment criteria are likely to attract multiple interested parties.

Geographic variations in demand growth suggest opportunities in specific markets. Melbourne's 23% increase in enquiries across 90% of suburbs indicates broad-based recovery momentum, while Darwin's 50% surge in buyer interest reflects the outsized opportunities available in smaller but affordable markets.

The timing considerations are particularly important given the October 1st implementation of the expanded First Homebuyer Guarantee. Investors positioning themselves in August and September may benefit from current supply constraints before additional buyer competition enters the market.

Godfrey Dinh, CEO of Futurerent, sees investment opportunities in the current environment: "We're witnessing a rare convergence of positive factors. Seventh consecutive month of growth, auction clearances at 76.3%, and inflation at 2.1%. With the expanded First Homebuyer Guarantee bringing unlimited buyers into the market from October 1st, investors who position themselves now could benefit from both current momentum and the demand wave that's coming."

Market Outlook

The outlook for Australian property markets through the remainder of 2025 remains constructively positive, supported by multiple tailwinds that are likely to sustain growth momentum well into the new year.

Additional interest rate cuts are highly likely, with economists expecting quarterly reductions that will continue to improve borrowing capacity and buyer sentiment. The current cash rate of 3.60% remains well above the stimulatory levels that characterised the pandemic period, providing scope for additional easing without creating excessive market heat.

Tim Lawless provides perspective on the growth trajectory: "I would be surprised if we saw the monthly rate of change in the national HVI getting anywhere near these earlier cyclical peaks, given how stretched housing affordability has become. What is more likely is that home values will rise at a more sustainable pace, with demand dampened by affordability constraints, more normal rates of population growth and cautious lending policy."

The spring selling season traditionally brings increased listing volumes, which will test the depth of current buyer demand. However, with enquiries per listing at multi-year highs and consumer sentiment reaching 3½ year peaks, the market appears well-positioned to absorb additional stock without significant price moderation.

SQM Research managing director Louis Christopher expects acceleration: "I think it's only a matter of time before we see an acceleration in housing price growth. Indeed, we're expecting it for the remainder of this year, and that's on the back of the multiple interest rate cuts, plus the bringing forward of the 5 per cent home deposit incentive."

The rental market's continued tightness, with vacancy rates at 1.5%, provides additional support for property investment fundamentals. As Christopher notes: "Renters who've essentially had enough of the rental increases over the years in what's still an elevated rental market would be biting at the bit to jump into the housing market if they can."

Australia's housing shortage reflects deeper structural challenges that extend well beyond current listing deficits. The nation's population is forecast to grow from 27.6 million to over 30 million residents by 2030, creating demand for approximately 2.4 million additional homes over the next five years. This demographic pressure occurs against a backdrop of persistently constrained construction activity, with current building rates falling well short of what's required to house this population growth. This structural demand foundation provides ongoing support for property values. For property investors, understanding this medium-term demographic trend helps explain why supply constraints are likely to persist well beyond typical market cycles, creating sustained support for both capital growth and rental demand across Australian markets.

Godfrey Dinh adds: "With quarterly rate cuts now delivering and borrowing capacity improving, we're seeing clients move decisively ahead of spring. Melbourne's recovery momentum and Brisbane's march toward $1 million median present clear opportunities for investors who can access capital and move with confidence."

How Futurerent Can Help

Spring represents the most active period in Australia's property calendar, but for many investors, accessing the capital needed to secure their next opportunity means months of refinancing paperwork, credit applications, and bank approvals.

Property investors know that prices grow faster than you can save. And even with a foot on the property ladder, taking the next step shouldn't mean asking the bank's permission or signing up to another lifetime of interest when all you need is to unlock what's already yours.

What if you could access that equity without refinancing, selling the property, or waiting until it's too late?

That's why investors turn to Futurerent - to unlock their equity without the usual trade-offs. There's no refinancing, no painful paperwork, and no impact on your credit score.

Futurerent helps investors cash out up to $100,000 per property, with funds in your account in just 2 business days. The property returns the cash out from a fixed portion of the rent over 3 years.

With market conditions suggesting buying opportunities ahead, having access to capital could make all the difference in securing your next investment before prices potentially move higher.