Nearly half of Australia's suburbs are now worth more than they've ever been – with 44.8% of suburbs sitting at record highs and another 329 within touching distance of their peaks.

In dollar terms, Australia's $11.5 trillion in residential wealth now represents 55.9% of total household wealth, backed by conservative leverage of just 21%.

The momentum is accelerating. Last weekend’s auction clearance rates held above 70% for five consecutive weeks, while construction starts just hit their highest level since June 2022. With major banks forecasting up to four rate cuts by early 2026, the fundamentals are aligning for continued growth – though not without challenges.

Key Highlights

- $11.5 trillion residential wealth representing 55.9% of total household wealth

- Outstanding mortgages just $2.4 trillion = comfortable 21% national LVR

- National values up 0.6% in June, and up 1.4% in Q2 (accelerating from 0.9% in Q1)

- 44.8% of 3,722 suburbs at record highs, with 329 more within 0.5% of peaks

- Brisbane leads with 78.8% of suburbs at peaks, Melbourne presents opportunity at 12.9%

- Dwelling-to-income ratio heading to 8.4 times nationally (from current 7.9x)

- Sydney clearance rate hits 76.2% – equal to February's year-high

- Construction starts reach 47,645 – highest quarterly total since June 2022

- First home buyer inquiries up 53% in past two months

- Rental growth moderates to 3.4% annually (down from 9.7% peak)

National Growth Momentum

The achievement of 44.8% of suburbs reaching record highs – with another 329 within touching distance – signals the breadth of this recovery phase. Cotality's analysis of 3,722 suburbs shows this proportion is expected to climb above 50% in coming months as momentum builds nationally.

What's particularly encouraging? Another 329 suburbs sit within 0.5% of their previous peaks, with 290 of those recording gains over the June quarter. The mathematics suggest we'll see the majority of Australian suburbs at record levels within the next few months.

The regional breakdown tells fascinating stories. Brisbane and Regional Queensland absolutely dominate with 78.8% and 77.7% of suburbs at peaks respectively. Perth continues its stellar run at 74.8%, while Adelaide (61.4%), Regional SA (58.8%) and Regional WA (53.6%) all show majority suburbs at or approaching records.

Melbourne presents the most interesting contrast. With only 12.9% of suburbs at record highs, it's clearly lagging – but that might be the opportunity for investors. As Cotality Economist Kaytlin Ezzy notes: "While this might be received as bad news for homeowners, prospective buyers in these markets are in the position to access housing at prices lower than they were three years ago."

The extremes are striking. In Canberra, only eight markets sit at peak, while Hobart has just one suburb (Brighton) at record highs. These disparities won't last forever.

The $11.5 Trillion Foundation

Let's talk about wealth for a moment. Australia's residential property is now valued at $11.5 trillion – a figure so large it's hard to comprehend. To put it in perspective, this represents 55.9% of total Australian household wealth. More than half of everything we own as a nation is tied up in the homes we live in.

What's remarkable is how conservatively this wealth is leveraged. Outstanding mortgages total just $2.4 trillion against this massive asset base, creating a national loan-to-value ratio of only 21%. This isn't the precarious, over-leveraged market some pessimists suggest – it's a wealth foundation built on solid equity.

This conservative positioning explains why neither banks, government, nor the RBA want significant property corrections. The systemic importance extends far beyond individual wealth – property underpins banking stability, government revenues through stamp duty and land tax, and the consumer confidence that drives our broader economy.

Tim Lawless from Cotality captures the opportunity this creates: "[Home owners and investors have] been able to build up equity in their home [and are] probably in a much better situation where they'll find access to upgrading or downsizing more straightforward, simply because they've had the benefit of time in the market."

"With national LVR at just 21% and $2.4 trillion in mortgages against $11.5 trillion in assets, as we move into a declining interest rate environment, Australian property owners have never been in a stronger position. This equity buffer creates options – whether that's helping kids buy their first home, adding to investment portfolios, or simply enjoying the security," says Godfrey Dinh, CEO of Futurerent.

Auctions Defy Winter Blues

You'd think school holidays and the RBA's surprise rate hold would dampen auction activity. Think again. The national clearance rate of 72.2% marks five consecutive weeks above 70%, sitting just shy of the year's 74.5% peak.

Sydney delivered the standout performance with a 76.2% clearance rate – equal to February's year-high – from 578 auctions. That's actually up from 560 auctions the same week last year, showing growth despite the winter timing. Melbourne remained the busiest market with 630 auctions achieving a solid 70.5% clearance rate.

The Agency's Michael Wood captured the mood perfectly: "The market is very in tune with the current rate. There's very good demand from all aspects of the market, first-time buyers, even investors are coming back, with interstate investment as well."

What's driving this strength? Michael Wood has a theory about the rate hold impact: "Any future rate cut would propel the market even further." In other words, buyers aren't waiting – they're moving now to beat the inevitable competition when cuts arrive.

Regional strength deserves special mention. Ray White Victoria's Jeremy Tyrrell reports: "Competition continued to dominate across the state. We saw midweek auctions really firing too. Our Ballarat team sold nine of 10 properties on Tuesday night alone."

Among smaller capitals, Adelaide posted impressive results with 75.6% clearance from 75 auctions – well above its 67.3% year-to-date average. Brisbane maintained momentum while Perth continued its remarkable run.

SQM Research's Louis Christopher sees acceleration ahead: "Prices are rising in my view. They're not galloping yet. I think come the next rate cut, it's going to happen, and we'll see a lot of buyers enter the market. We are getting close to some more accelerated housing price rises, but we're not quite there yet."

Construction Gains Momentum

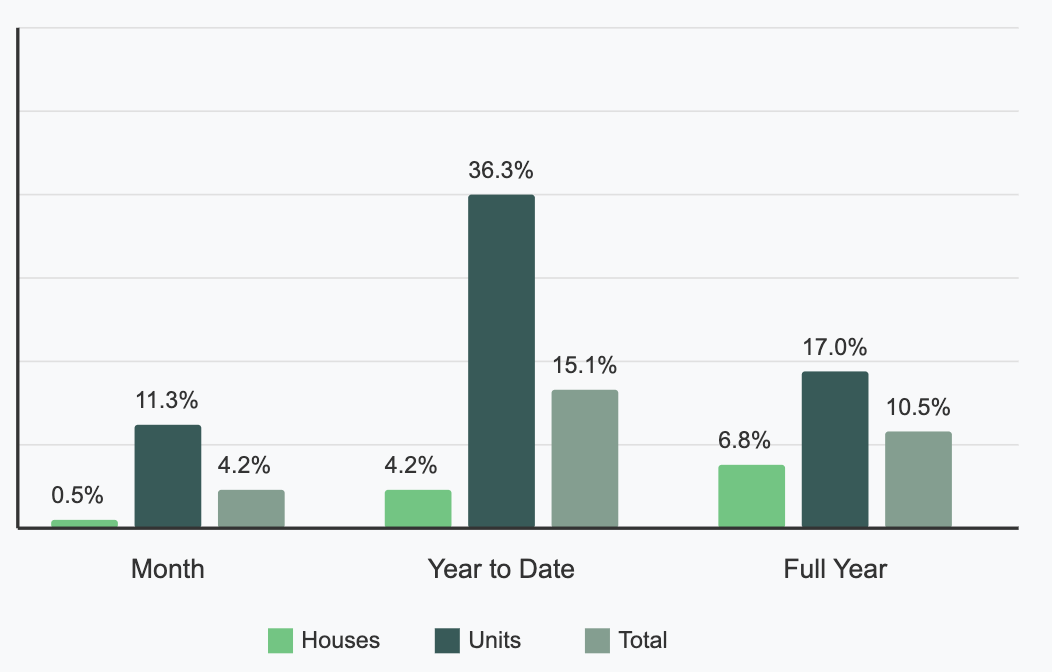

Here's some positive news on the supply front. Construction starts hit 47,645 in the March quarter – the highest since June 2022. That's an impressive 17.3% jump year-on-year and suggests the industry's worst days might be behind us.

The composition reveals evolving preferences. Private house commencements rose a modest 6.3% to 27,923, but the real action was in higher-density housing. Other residential starts – your units, townhouses, and semis – surged 21.8% to 18,161. This shift toward density makes sense given affordability pressures, land shortages, and changing lifestyle preferences.

May's building approvals added to the positive momentum with a 3.2% rise to 15,212, rebounding from April's decline. Again, apartments and townhouses led the charge with an 11.3% monthly jump, while detached houses remained essentially flat at 0.5%.

ABS National Building Approvals Seasonally Adjusted

May 2025

But let's keep perspective. We're still running at 183,000 annual approvals when we need 240,000 to meet Housing Accord targets. To hit the government's ambitious 1.2 million homes by 2029, we need 60,000 new homes per quarter. At 47,645, we're running about 25% short.

Master Builders Australia's Denita Wawn acknowledges both progress and challenge: "While there is room for optimism that the worst is now behind us, the government and industry need to play catch-up if we're going to meet the 1.2 million new homes target."

Home Building - Capitals Trend Down 29.8% since 2016 Peak

ABS Monthly Capital City Annual Dwelling Building Approvals

The completion challenge adds another wrinkle. Despite strong starts, completions actually fell 4.4% to 43,517. RSM Australia's Devika Shivadekar explains: "While the sector is successfully initiating new projects and maintaining strong commencement activity, it's clear the industry is still battling completion timelines."

Long-term trends remain concerning. Capital city approvals sit 29.8% below their 2016 peak, while unit approvals have collapsed 48.4% from those heady days. And remember – approval doesn't mean immediate construction. Houses take over a year to build, apartment projects typically three years or more.

"The combination of 47,645 construction starts – the highest in three years – with stock levels 16.7% below average and a recent market bias against buying off-the-plan, creates compelling conditions for investors" notes Godfrey Dinh, CEO of Futurerent.

The Renovation Renaissance

While we wait for new supply, existing homeowners are discovering renovation opportunities. National house prices rose 4.3% over the past year while building costs increased just 2.9% – creating an expanding profit margin for well-executed upgrades.

Tim Lawless spots the trend: "We're starting to hear a lot of anecdotes that trades are becoming a little more available. It looks like construction costs are finding their groove once again, rising at around average levels."

Melbourne offers particular promise for renovators. As Lawless explains: "I would suggest that Melbourne's got some great opportunities, simply because it's got a lower price point to buy into the market. It helps to de-risk the value-add if you've got a lower price point."

Affordability Reality Check

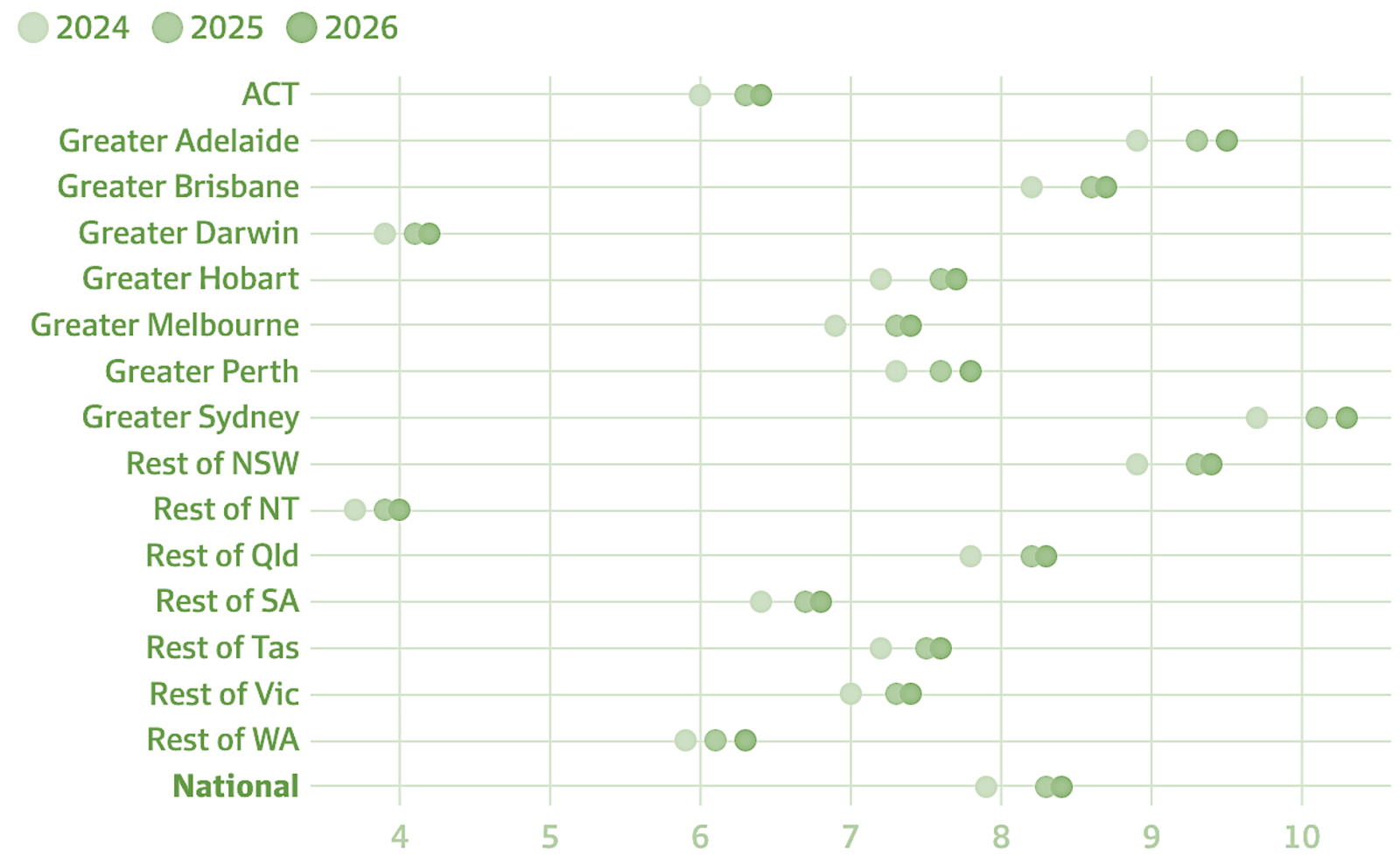

Now for the sobering news that deserves our full attention. Australia's dwelling-to-income ratio hit 7.9 times typical household income in December 2024. By next year, Cotality projects this could stretch to 8.4 times – the highest dwelling-value-to-income ratio since at least 2021.

Greater Sydney stands as the extreme example of this affordability challenge. The harbour city's dwelling value to income ratio sits at 9.7 times – already confronting for new buyers. But here's what should really catch your attention: this could surge to a whopping 10.3 times by the end of next year, surpassing even the 10.2 peak reached in 2022.

The Sydney mathematics are stark. As of December 2024, Greater Sydney's median dwelling value sits at about $1.184 million. Against this, the average household income is $2,355 a week. Do the sums and you'll see why first-home buyers are increasingly turning to family assistance or alternative strategies.

At the other end of the spectrum, regional Northern Territory offers the nation's most affordable entry point, where a home costs about 3.7 times household income.

Cotality's Tim Lawless sees this trend continuing: "Property values will continue rising faster than household incomes, increasing the dwelling-value-to-income ratio across capital cities and the regions." It's a structural shift that advantages existing owners while challenging new entrants.

Australian Dwelling-to-Income Ratios (x)

For existing owners, this affordability pressure paradoxically creates wealth. Since February's first rate cut, property values jumped 2.3% – that's an $18,000 gain on the median dwelling in just five months. The mathematics are simple: as affordability stretches for new buyers, scarcity value increases for existing properties.

The response? Adaptation and innovation. The "bank of mum and dad" has moved from embarrassment to mainstream necessity. "Rentvestors" – those buying investment properties while continuing to rent where they want to live – represent a rapidly growing segment. As DeBondt-Barker explains: "They know they can get in the property market somewhere else and then rent. Hopefully, if they do it wisely, they make some money and then buy their home."

Rate Cut Roadmap Becomes Clearer

Following the RBA's surprise hold, all four major banks have updated their forecasts – and they're unanimous that cuts are coming. The only debate is how many and how fast.

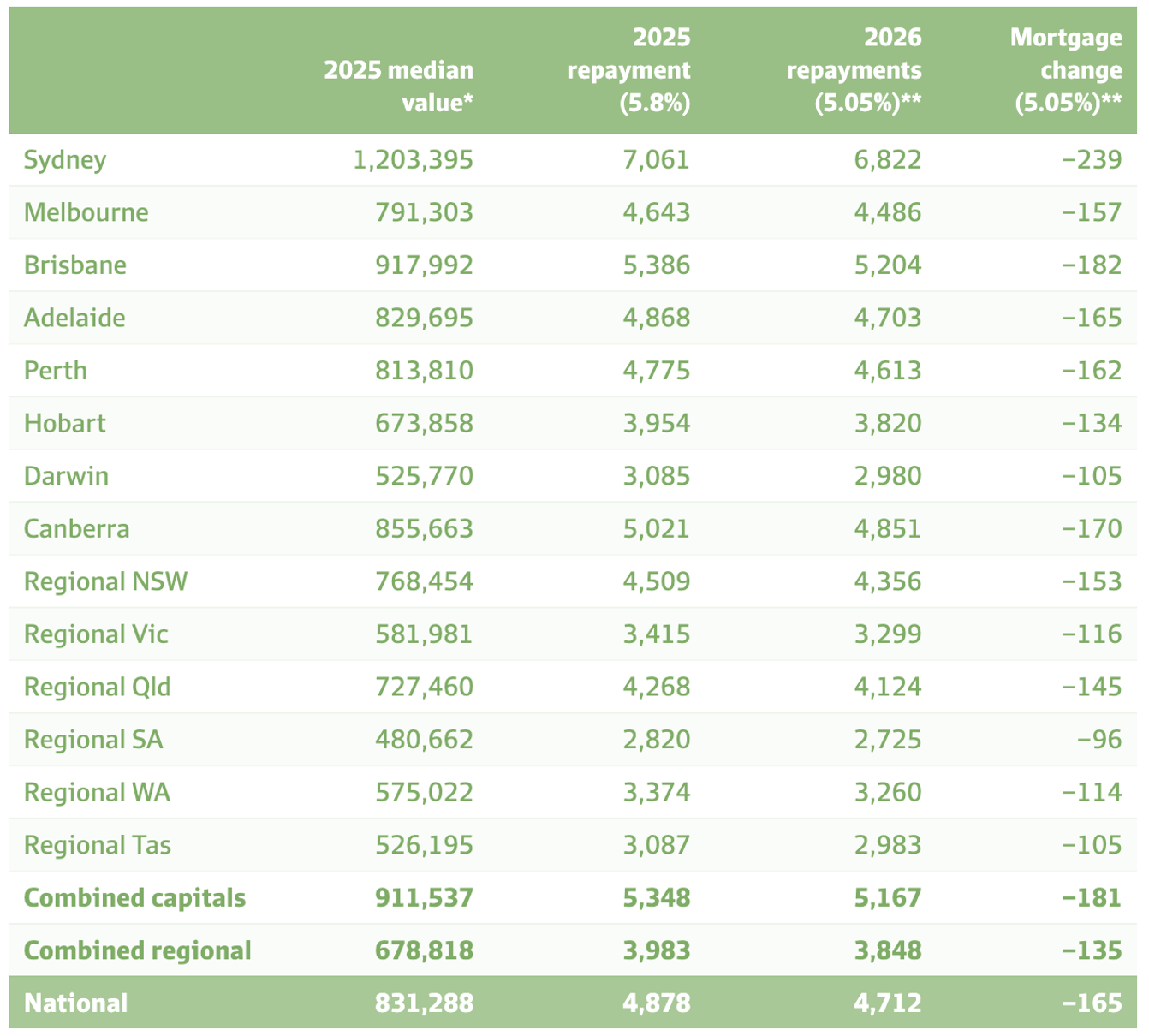

Commonwealth Bank and ANZ see two cuts delivering a 3.35% cash rate by year-end. NAB goes further with three cuts reaching 3.10% by February 2026. Westpac wins the optimism prize with four cuts potentially hitting 2.85% by May 2026.

The impact on mortgage repayments tells the real story of what's ahead. Based on projected rate movements, a typical Sydney borrower could see monthly repayments drop by $239, while even regional borrowers would save over $100 monthly – meaningful relief that will flow directly into borrowing capacity and market activity.

Dwelling values and monthly mortgage repayments in 12-months ($)

* From May 2025 ** Derived mortgage rate

Assumptions: Mortgage rate is based on average outstanding rate for owner-occupier loans with a principal-and-interest repayment period of 30yrs. Assumes changes to cash rate are passed on in full.

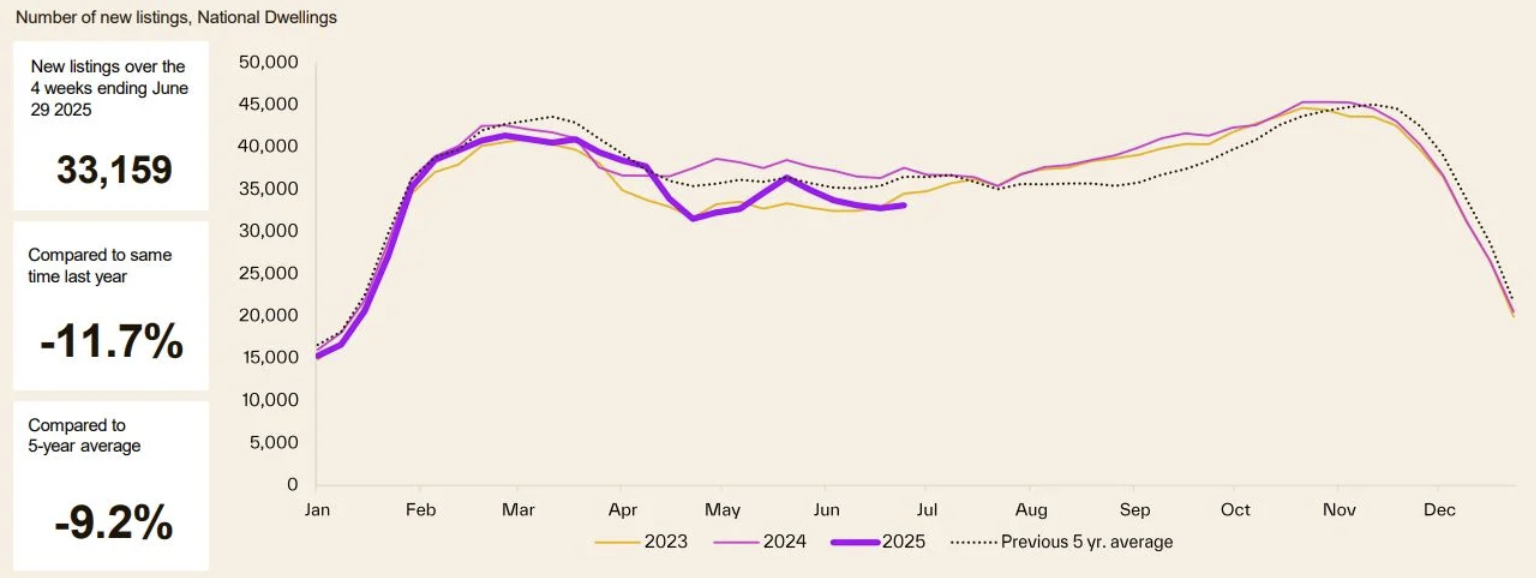

Supply Squeeze Continues

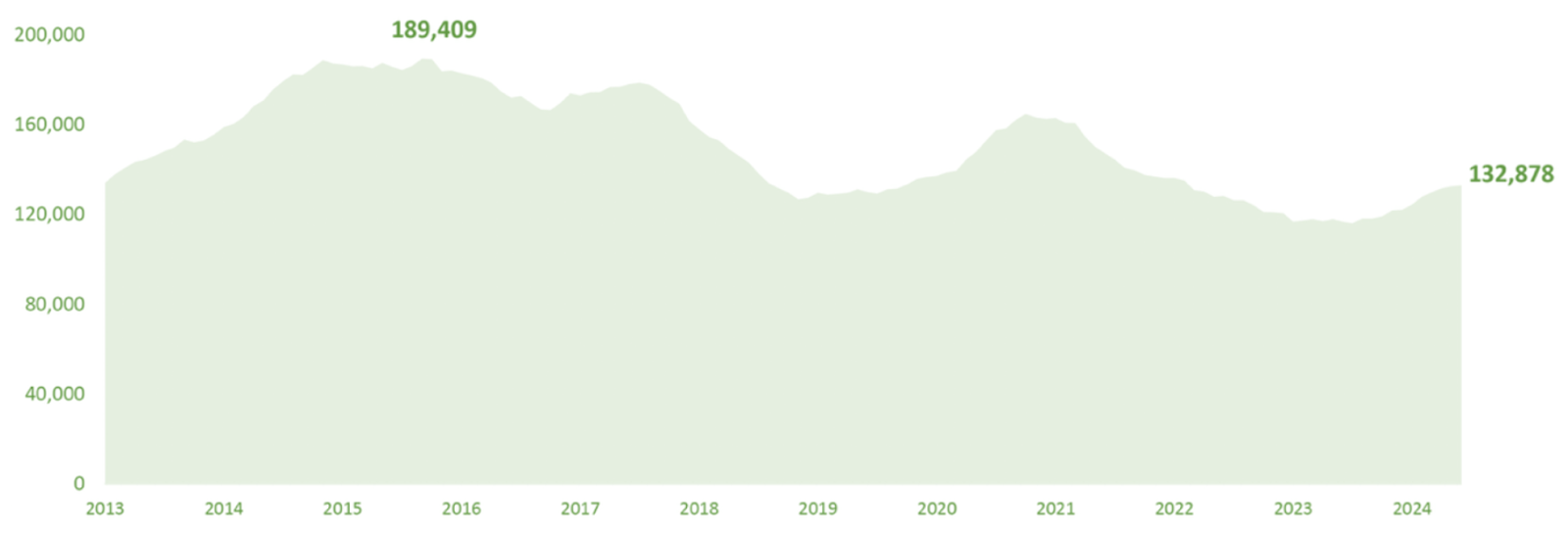

Despite construction improvements, the fundamental supply shortage persists. New listings totalled just 33,159 properties nationally in the four weeks to June 29th – down 11.7% year-on-year and the lowest for this time of year since 2020.

Total stock sits at 127,020 properties, down 16.7% from five-year averages. Industry veterans note another problem: quality properties remain particularly scarce. Owners of A-grade homes and investment-grade properties simply aren't selling.

Number of new listing, National Dwellings

The rental market reinforces these constraints. Despite growth moderating to 3.4% annually (from the 9.7% peak), vacancy rates remain critically tight at 1.6% – well below the 3% considered healthy. Properties now take 35 days to sell, up from 29 days last year, suggesting buyers are becoming more selective even as competition intensifies.

"Those waiting for supply solutions to moderate price growth will be waiting a long time" observes Godfrey Dinh, CEO of Futurerent. "Even with 47,645 commencements this quarter, immigration continues to outpace this. With stock already 16.7% below average and quality properties particularly scarce, today's supply constraints will persist well into 2027-2028."

Strategic Positioning

The convergence of record suburbs, construction recovery, and impending rate cuts creates a market requiring strategic thinking. Traditional approaches – buying yesterday's winners – may prove less effective than identifying tomorrow's opportunities.

Melbourne's lag presents obvious potential. With only 12.9% of suburbs at peaks versus Brisbane's 78.8%, mean reversion suggests catch-up growth ahead. Lower entry costs reduce risk while Victoria's population growth supports medium-term demand.

Interstate diversification makes increasing sense as performance gaps widen. The growing "rentvestor" trend reflects this reality – buying where value exists rather than where you want to live.

Moving before rate cuts means less competition but requires confidence in the trajectory. Waiting provides certainty but likely means paying more. The five consecutive weeks above 70% clearance rates suggest many have already chosen action over patience.

Market Outlook

Australia's property market has reached an inflection point where broad-based recovery meets emerging complexity. The 44.8% of suburbs at record highs will likely exceed 50% within months, but the next phase requires more nuanced navigation.

The building momentum is unmistakable. Quarterly growth accelerated from -0.1% in Q4 2024 to 0.9% in Q1 2025, then 1.4% in Q2. With June alone delivering 0.6% growth and rate cuts ahead, this trajectory points clearly upward.

Supply constraints ensure fundamental support through 2025-2026, even as the 47,645 quarterly construction starts represent meaningful improvement. The dwelling-to-income ratio approaching 8.4 times introduces sustainability questions, but existing owner equity and conservative lending standards provide stability.

Regional divergence will likely persist, creating distinct micro-markets within the national narrative. Melbourne's catch-up potential, Brisbane's momentum, Perth's continued strength, and Sydney's premium positioning each offer different risk-reward equations.

This growing divide explains the surge in first-home buyer activity. Property Home Base reports a 40% increase in inquiries over the financial year, with a remarkable 53% surge in just the past two months. Founding director Julie DeBondt-Barker confirms: "First-home buyers are out there in force. Demand is really, really acute in Victoria, but it's also in South Australia and Queensland."

For investors, success increasingly depends on strategic selection rather than market timing. The broad recovery provides rising tide benefits, but the real opportunities lie in understanding which suburbs among those 329 approaching peaks will break through next, which lagging markets offer value, and how rate cuts will reshape competitive dynamics.

Bank of Queensland's Peter Munckton suggests "a 10 to 15 per cent price rise over the next two years is reasonable based on an analysis of 40 years of data." If he's right, today's prices will look attractive by 2027.

How Futurerent Can Help

Property investors know that prices grow faster than you can save. And even with a foot on the property ladder, taking the next step shouldn't mean asking the bank's permission or signing up to another lifetime of interest when all you need is to unlock what's already yours.

What if you could access that equity without refinancing, selling the property, or waiting until it's too late?

That's why investors turn to Futurerent - to unlock their equity without the usual trade-offs. There's no refinancing, no painful paperwork, and no impact on your credit score.

Futurerent helps investors cash out up to $100,000 per property, with funds in your account in just 2 business days. The property returns the cash out from a fixed portion of the rent over 3 years.

With market conditions suggesting significant opportunities ahead, having quick access to capital could make all the difference in securing your next investment before prices potentially move higher.